i

監査基準報告書 701 研究文書第3号

「監査上の主要な検討事項」における監査人の主要な見解等の記載に係る

海外事例の調査レポート(研究文書)

2024 年 11 月 1 2 日

日 本 公 認 会計士 協 会

監査・保証基準委員会

(研究文書:第 15 号)

頁

Ⅰ はじめに

1.本研究文書の概要 .............................................................. 1

(1) 公表の背景 .................................................................. 1

(2) 本研究文書の構成 ............................................................ 1

2.監査人の主要な見解等 .......................................................... 1

(1) 監査人の主要な見解等の記載に関する取扱い .................................... 2

Ⅱ 各国の調査概要

1.英国 .......................................................................... 3

(1) 英国における一般に公正妥当と認められる監査の基準 ............................ 3

(2) 英国における調査概要 ........................................................ 4

2.オランダ ...................................................................... 4

(1) オランダにおける GAAS ........................................................ 4

(2) オランダにおける調査概要 .................................................... 5

3.シンガポール .................................................................. 5

(1) シンガポールにおける GAAS .................................................... 5

(2) シンガポールにおける調査概要 ................................................ 6

4.米国 .......................................................................... 6

(1) 米国における GAAS............................................................ 6

(2) 米国における調査概要 ........................................................ 6

5.まとめ ........................................................................ 7

(1) 各国における調査結果まとめ .................................................. 7

(2) 調査結果総括 ................................................................ 7

Ⅲ 調査結果を踏まえた考察

1.監査人の主要な見解等の記載の有無の傾向 ........................................ 8

2.監査人の主要な見解等の記載内容の傾向 .......................................... 8

3.まとめ ........................................................................ 9

Ⅳ 監査人の主要な見解等の海外事例

海外事例1.結論の記載以外の付加的な情報がない事例 ................................ 11

ii

海外事例2.個別意見の表明であるような誤解を与える可能性のある事例 ................ 12

海外事例3.個別保証を付与していない点を明記している例 ............................ 14

海外事例4.監査人が識別した事項及びそれに対応する監査アプローチ .................. 15

海外事例5.監査委員会の監査報告書において強調した事項を記載した事例 .............. 16

【本研究文書は、一般に公正妥当と認められる監査の基準を構成するものではなく、会員が遵守す

べき基準等にも該当しない。また、2024 年 11 月 12 日時点の最新情報に基づいている。】

- 1 -

《Ⅰ はじめに》

《1.本研究文書の概要》

《(1) 公表の背景》

監査上の主要な検討事項(key Audit Matters:KAM)が上場会社等の監査に適用されて、2024 年

3月期で4年目を迎えた。

KAM については、金融庁、日本証券アナリスト協会、日本公認会計士協会等において、事例分析

を継続的に行っており、2022 年3月期における KAM について以下が公表されている。

・ 金融庁「監査上の主要な検討事項(KAM)の特徴的な事例と記載のポイント 2022」(2023 年2

月 17 日)

・ 日本証券アナリスト協会「証券アナリストに役立つ監査上の主要な検討事項(KAM)の好事例

集 2022」(2023 年2月 10 日)

・ 日本公認会計士協会「監査基準報告書 701 研究文書第2号「「監査上の主要な検討事項」の事

例分析(2021 年4月~2022 年3月期)レポート(研究文書)」(2022 年 12 月 26 日)

金融庁「監査上の主要な検討事項(KAM)の特徴的な事例と記載のポイント 2022」においては、

以下のコメントが紹介されている。

・ findings 等については、監査人の対応の結論が明確になるので、利用者側としても利便性が

高まる記載であると考えている。

・ findings 等の記載は、国際監査基準においても、我が国の監査基準報告書においても認めら

れており、かつ、海外において実際に行われ、グローバル・ネットワークの中ではそれを原則的

に要請しているところもある。我が国の監査人が findings 等の記載を行わない理由はないので

はないか。

本研究文書は、関係者における今後の key observations 及び findings(以下「監査人の主要な

見解等」という。)に関する議論の参考にすることを目的として、取りまとめを行ったものである。

《(2) 本研究文書の構成》

本研究文書では、国際監査基準(International Standards on Auditing:ISA)及び監査基準報

告書における監査人の主要な見解等の取扱いを説明した上で、KAM の実務が先行していると考えら

れる英国、オランダ、シンガポール及び米国における状況を調査し、その結果を「Ⅱ 各国の調査

概要」以降で取りまとめている。

なお、本研究文書作成に際しては、監査基準報告書 701 研究文書第2号「「監査上の主要な検討

事項」の事例分析(2021 年4月~2022 年3月期)レポート(研究文書)」で分析対象とした事例以

降の我が国の開示例については分析を行っていない。

《2.監査人の主要な見解等》

先行する海外の事例では「key observations」と「findings」の二つの用語が使用されている。

両者の内容は次のとおりであり、本研究文書でも「監査人の主要な見解等」として「key

observations」及び「findings」を扱っている。

- 2 -

・ key observations

監査基準報告書では、監査上の対応やアプローチについての監査報告書の利用者の理解を促

進させるため、KAM に対する監査上の対応として、主要な見解(key observations)を記載する

ことがある(監査基準報告書 701「独立監査人の監査報告書における監査上の主要な検討事項の

報告」の A46 項及び A47 項参照)とされており、ISA においても同様の取扱いとなっている。

なお、当該記載は適用指針であり、記載の要否は、監査人の判断によることとなっている(監

査基準報告書 700 実務ガイダンス第1号「監査報告書に係るQ&A」Q2-12 参照)。

・ findings

findings は、ISA 及び監査基準報告書において明確に定義されているわけではないが、海外

の一部の実務において findings の見出しを付して、監査上の発見事項(監基報 701 の A60 項参

照)を記載している事例がある。

《(1) 監査人の主要な見解等の記載に関する取扱い》

KAM の記載に当たっては、ISA 及び監査基準報告書において、次の点に留意することが適切であ

るとしている(監基報 701 の A47 項参照)。

・ 財務諸表に対する意見を監査人が形成する上で、当該事項への対応を監査人が適切に完了し

ていないという印象を与えない。

・ 汎用的な又は標準化された文言を避け、当該事項を企業の具体的な状況に直接関連付ける。

・ 財務諸表に関連する注記事項がある場合、その内容を考慮する。

・ 財務諸表に含まれる個別の事項に対する意見を表明しない、又は表明しているという印象を

与えない。

4点目の留意事項については、実務ガイダンスで、監査人の主要な見解等を記載するに当たっ

ては、関連する勘定残高等についての結論を述べるのではなく、監査上の対応として記載した監

査アプローチ又は手続の対象となった要素(経営者の重要な仮定等)に対する監査人の評価を記

述すること等が留意点となると補足されている(監基報 700 ガ1Q2-12 参照)。

なお、我が国においては、監査人の主要な見解等の開示例は見られていない。

- 3 -

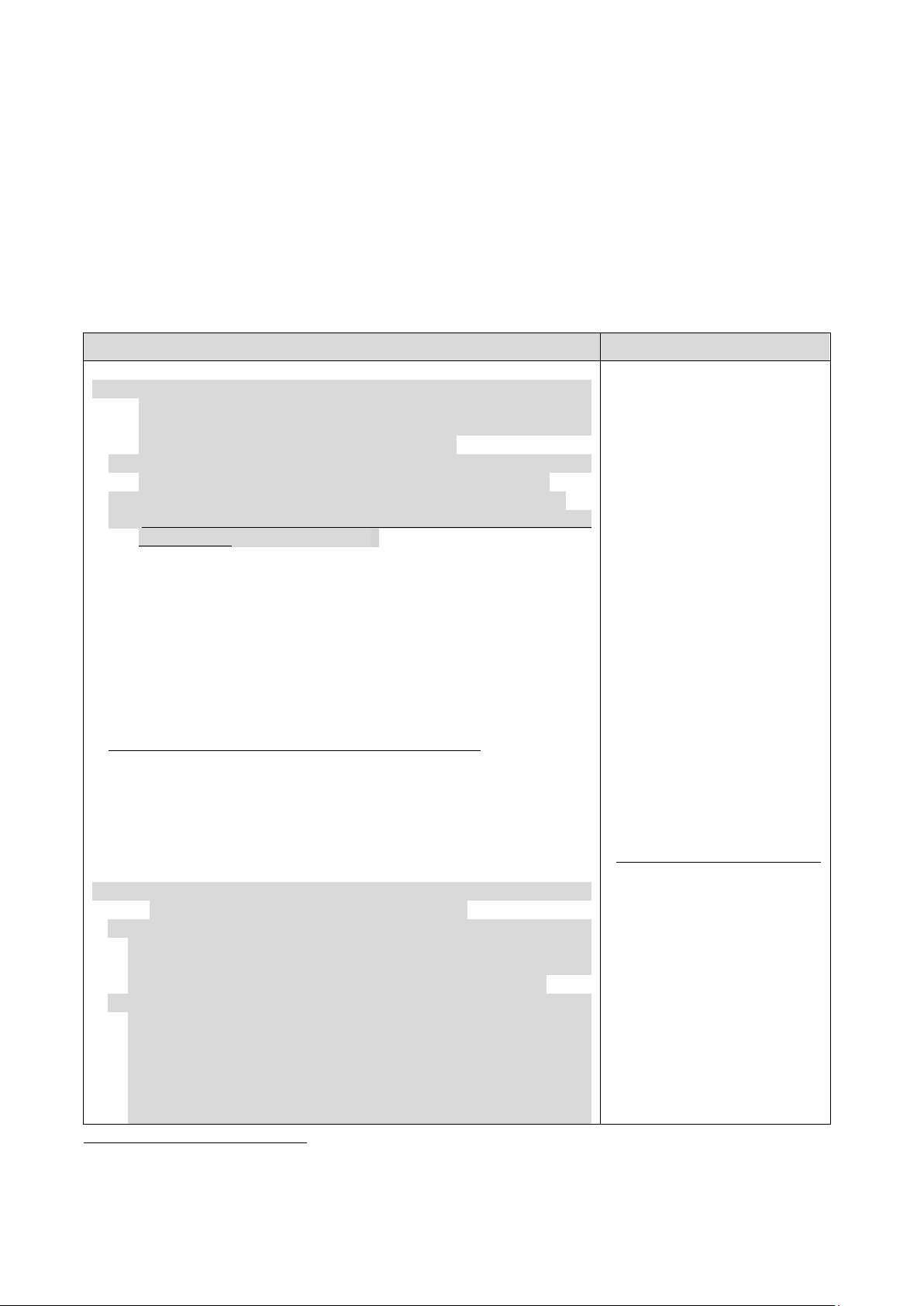

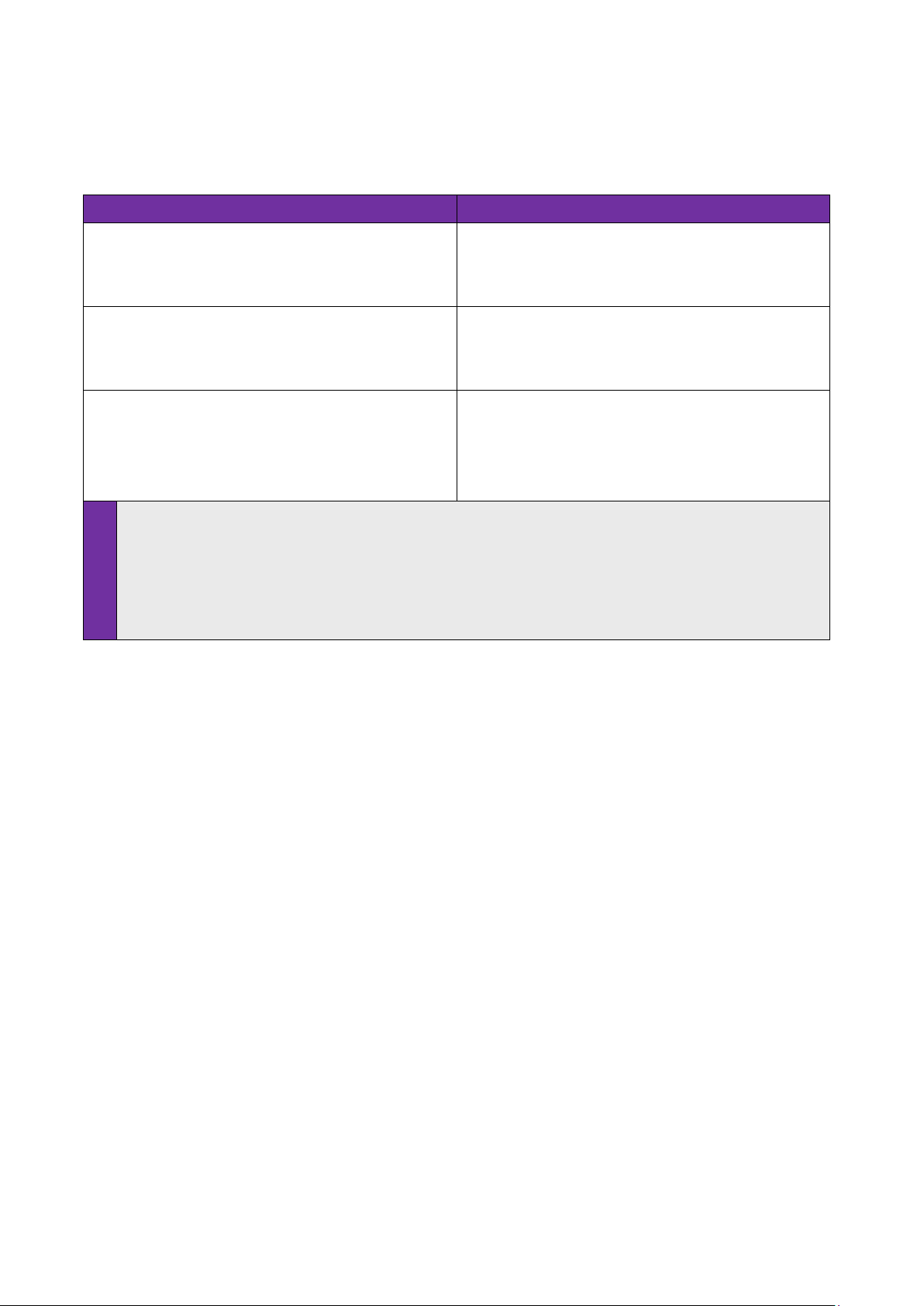

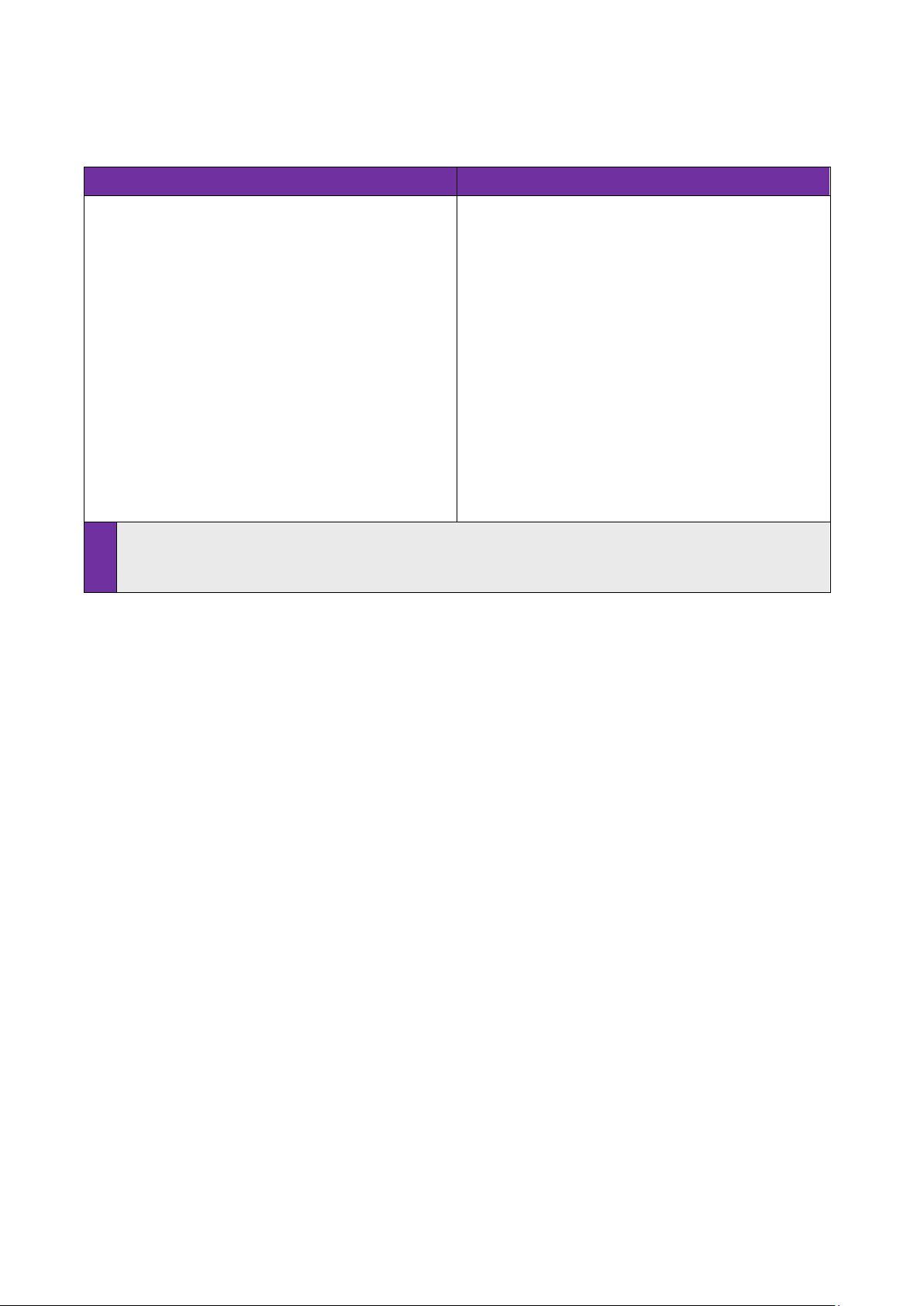

《Ⅱ 各国の調査概要》

《1.英国》

《(1) 英国における一般に公正妥当と認められる監査の基準》

英国 と 日 本 の 一 般 に 公 正 妥 当 と 認 め ら れ る 監 査 の 基 準 ( Generally Accepted Auditing

Standards:GAAS)を比較すると、英国には ISA(UK)701

1

における「where relevant, key

observations arising with respect to those risks」という要求事項がある点が異なる。この

要求事項の存在により、英国においては、主要な見解(key observations)が記載されている事例

が一定数程度存在すると考えられる。

英国 日本(参考)

【ISA(UK)701】(グレー部分は英国独自の規定)

13-1. For audits of financial statements of public interest

entities, in describing each of the key audit matters in

accordance with paragraph 13, the auditor's report shall

provide, in support of the audit opinion:

(a) A description of the most significant assessed risks of

material misstatement, (whether or not due to fraud);

(b) A summary of the auditor's response to those risks; and

(c) Where relevant, key observations arising with respect to

those risks. (Ref: Para. A51-1)

(省 略)

A46. The amount of detail to be provided in the auditor’s report

to describe how a key audit matter was addressed in the audit

is a matter of professional judgment. In accordance with

paragraph 13(b), the auditor may describe:

・ Aspects of the auditor’s response or approach that were most

relevant to the matter or specific to the assessed risk of

material misstatement;

・ A brief overview of procedures performed;

・ An indication of the outcome of the auditor’s procedures; or

・ key observations with respect to the matter,

or some combination of these elements.

Law or regulation or national auditing standards may

prescribe a specific form or content for the description of

a key audit matter, or may specify the inclusion of one or

more of these elements.

(省 略)

A51-1. In meeting the requirement of paragraph 13-1(c), the

auditor takes into account the following:

・ 'Where relevant' means where an auditor has identified an

issue that they consider would be of relevance to the users

of the financial statements. In planning their audit, the

auditor will have considered the user perspective; and

・ A ‘key observation’ is the conclusion drawn by the auditor

in respect of a key audit matter or an indication of the

outcome of the auditor‘s procedures. In reporting on key

observations, the auditor should be careful not to give the

impression that a separate opinion is being conveyed on a key

audit matter and not to do so in a manner that would undermine

the auditor's opinion on the financial statements as a whole.

【監査基準報告書 701】

(該当する要求事項なし)

A46.監査上の対応に関する記載の

詳細さの程度は、監査人の職業

的専門家としての判断に係る事

項である。監査人は、第 12 項(4)

に基づき、監査上の対応につい

て以下のいずれか、又は組み合

わせて記載する。

・ 監査上の主要な検討事項に

最も適合している、又は評価し

た重要な虚偽表示リスクに焦

点を当てた監査人の対応又は

監査アプローチの内容

・ 実施した手続の簡潔な概要

・ 監査人による手続の結果に

関連する記述

・ 当該事項に関する主要な見解

(該当する記載なし)

1

https://www.frc.org.uk/library/standards-codes-policy/audit-assurance-and-ethics/auditing-standards/isa-

uk-701/

- 4 -

《(2) 英国における調査概要》

・ 調査対象の抽出

ロンドン証券取引所(London Stock Exchange:LSE)上場企業のうち、本社所在地が英国であ

る企業 100 社を無作為に抽出した上で、それらの企業の KAM を調査し、監査人の主要な見解等

の記載の有無及び記載がある場合はその内容の分析を行った。

・ 調査結果概要

56%の企業において主要な見解(key observations)又は見解(observations)が記載されて

おり、一部の企業(4社)において findings が記載されていた。

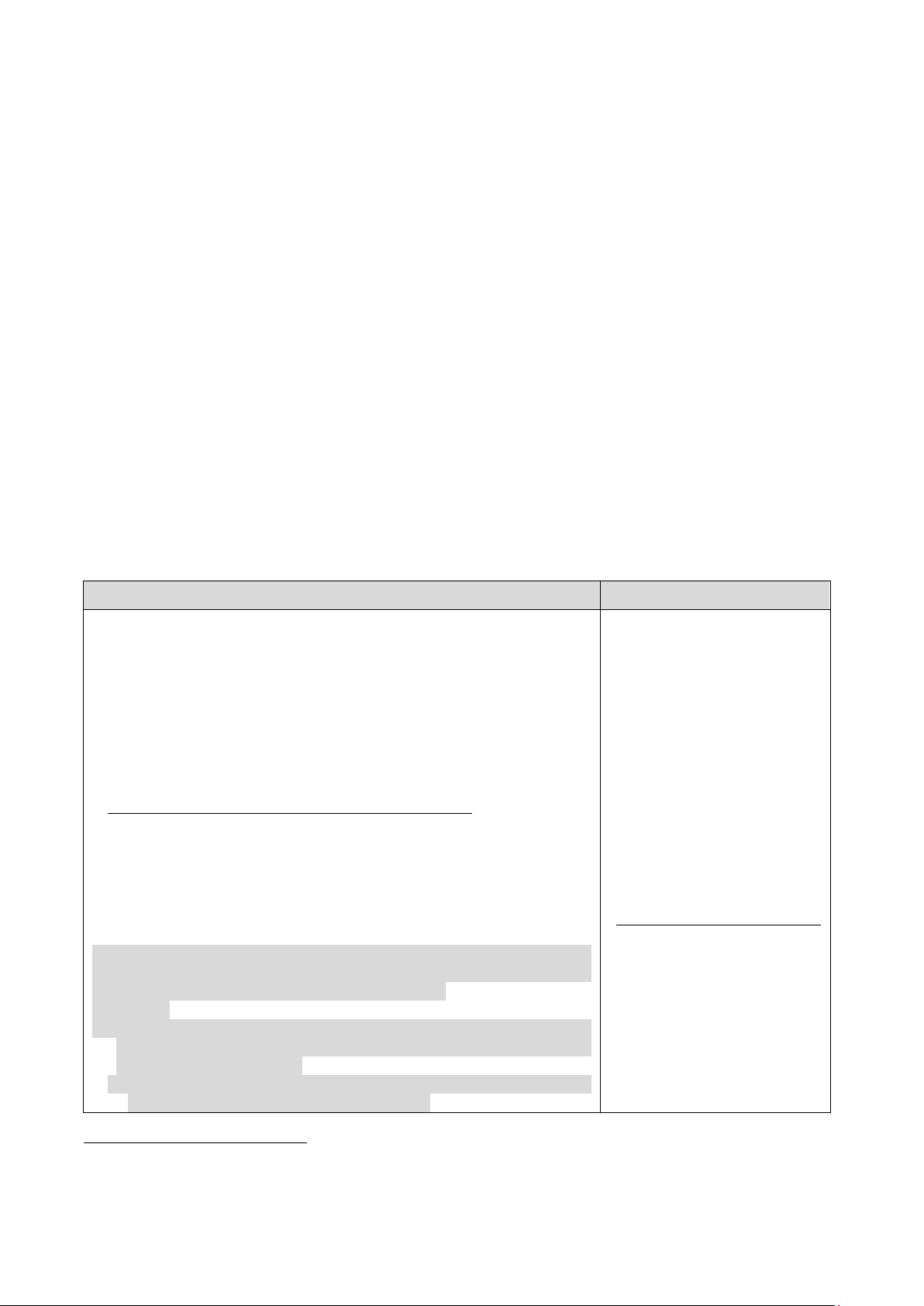

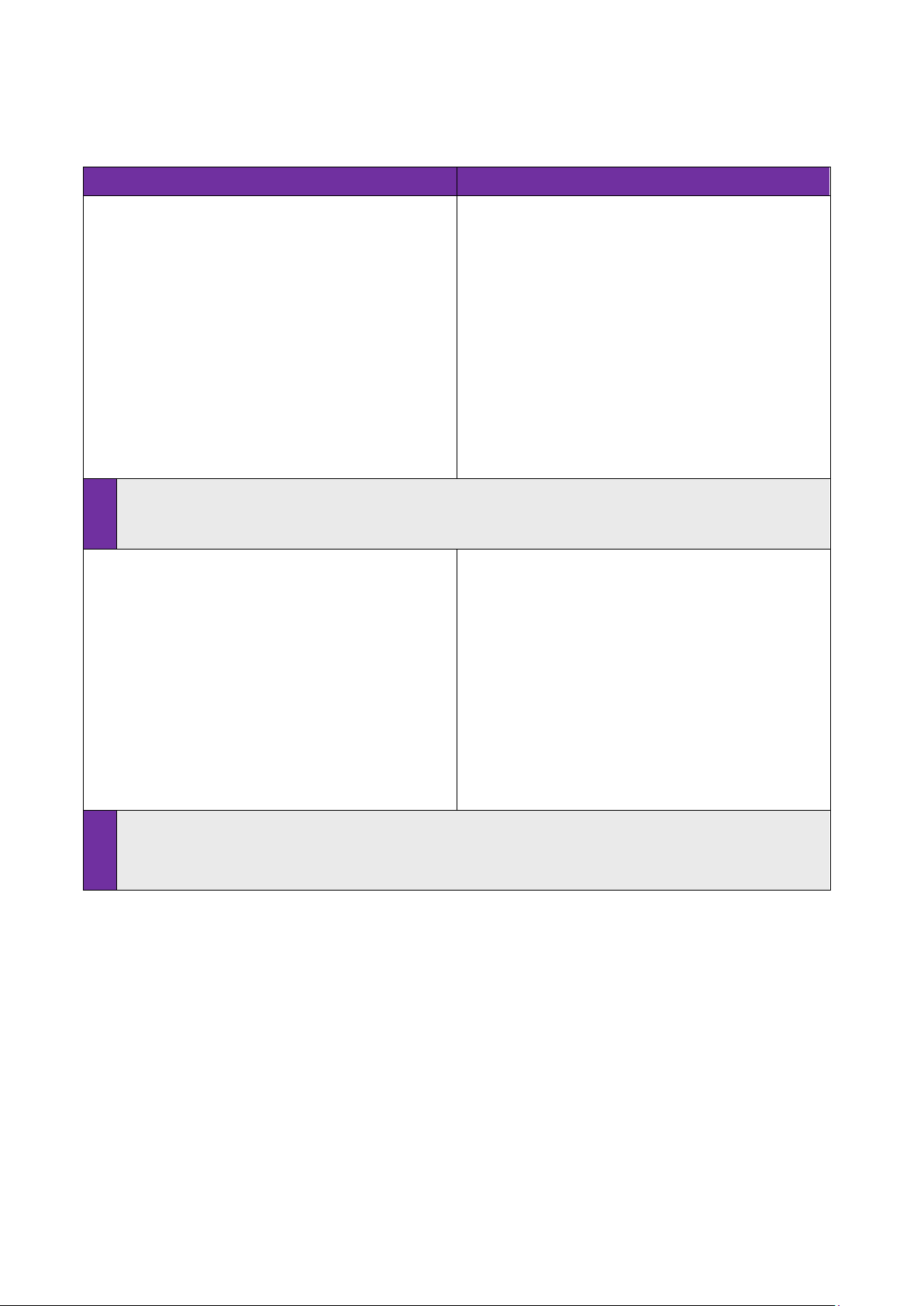

《2.オランダ》

《(1) オランダにおける GAAS》

オランダと日本の GAAS を比較すると、オランダにおいては社会的影響度の高い事業体(Public

Interest Entity:PIE)の法定監査に関する規則において「where relevant, key observations

arising with respect to those risks」という要求事項がある点が日本と異なる。この要求事項

の存在により、オランダにおいては、主要な見解(key observations)が記載されている事例が一

定数程度存在すると考えられる。

オランダ 日本(参考)

【ISA701(オランダでは ISA を修正なしで適用

2

)】

A46. The amount of detail to be provided in the auditor’s report

to describe how a key audit matter was addressed in the audit

is a matter of professional judgment. In accordance with

paragraph 13(b), the auditor may describe:

・Aspects of the auditor’s response or approach that were most

relevant to the matter or specific to the assessed risk of

material misstatement;

・A brief overview of procedures performed;

・An indication of the outcome of the auditor’s procedures; or

・key observations with respect to the matter,

or some combination of these elements.

Law or regulation or national auditing standards may

prescribe a specific form or content for the description of

a key audit matter, or may specify the inclusion of one or

more of these elements.

(グレー部分はオランダ独自の規則)

【Regulation (EU) No 537/2014 of the European Parliament and of

the Council of 16 April 2014 on specific requirements regarding

statutory audit of public-interest entities

3

】

Article 10

2. The audit report shall be prepared in accordance with the

provisions of Article 28 of Directive 2006/43/EC and in

addition shall at least:

(a) state by whom or by which body the statutory auditor(s) or

the audit firm(s) was (were) appointed;

【監査基準報告書 701】

A46.監査上の対応に関する記載の

詳細さの程度は、監査人の職業

的専門家としての判断に係る事

項である。監査人は、第 12 項(4)

に基づき、監査上の対応につい

て以下のいずれか、又は組み合

わせて記載する。

・ 監査上の主要な検討事項に

最も適合している、又は評価し

た重要な虚偽表示リスクに焦

点を当てた監査人の対応又は

監査アプローチの内容

・ 実施した手続の簡潔な概要

・ 監査人による手続の結果に

関連する記述

・ 当該事項に関する主要な見解

(該当する記載なし)

2

https://www.ifac.org/about-ifac/membership/members/royal-nederlandse-beroepsorganisatie-van-accountants

3

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014R0537&from

- 5 -

オランダ 日本(参考)

(b) indicate the date of the appointment and the period of total

uninterrupted engagement including previous renewals and

reappointments of the statutory auditors or the audit firms;

(c) provide, in support of the audit opinion, the following:

(i) a description of the most significant assessed risks of

material misstatement, including assessed risks of

material misstatement due to fraud;

(ii) a summary of the auditor's response to those risks; and

(iii) where relevant, key observations arising with respect

to those risks

《(2) オランダにおける調査概要》

・ 調査対象の抽出

欧州単一電子フォーマット(Altova European Single Electronic Format:ESEF)に基づき開

示を行っているオランダの上場企業のうち、英文開示を行っており、かつ、監査報告書を公表し

ている企業 80 社に対し、該当企業の KAM を調査し、監査人の主要な見解等の記載の有無及び記

載がある場合はその内容の分析を行った。

・ 調査結果概要

95%の企業において主要な見解(key observations)又は observations が記載されていた。

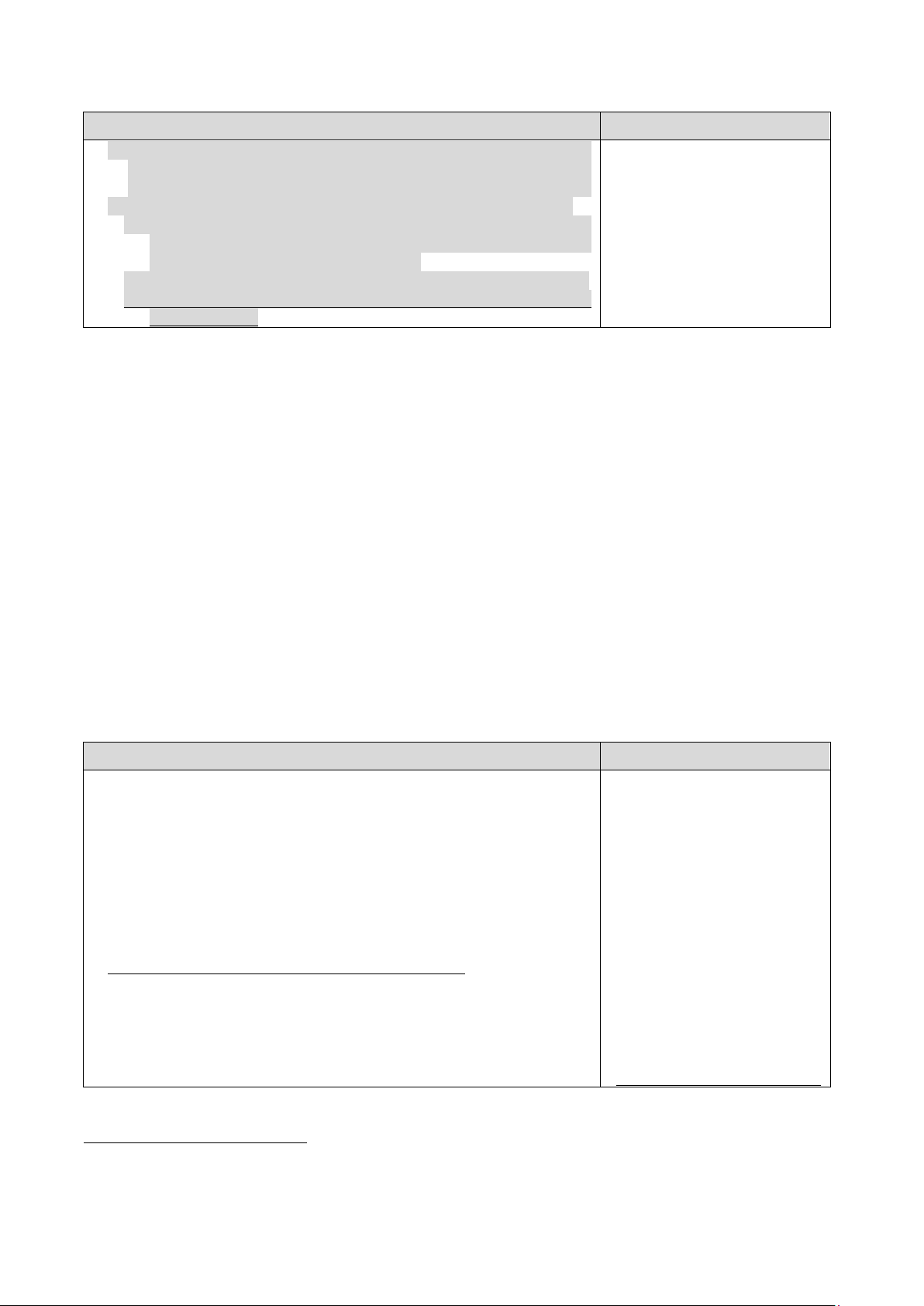

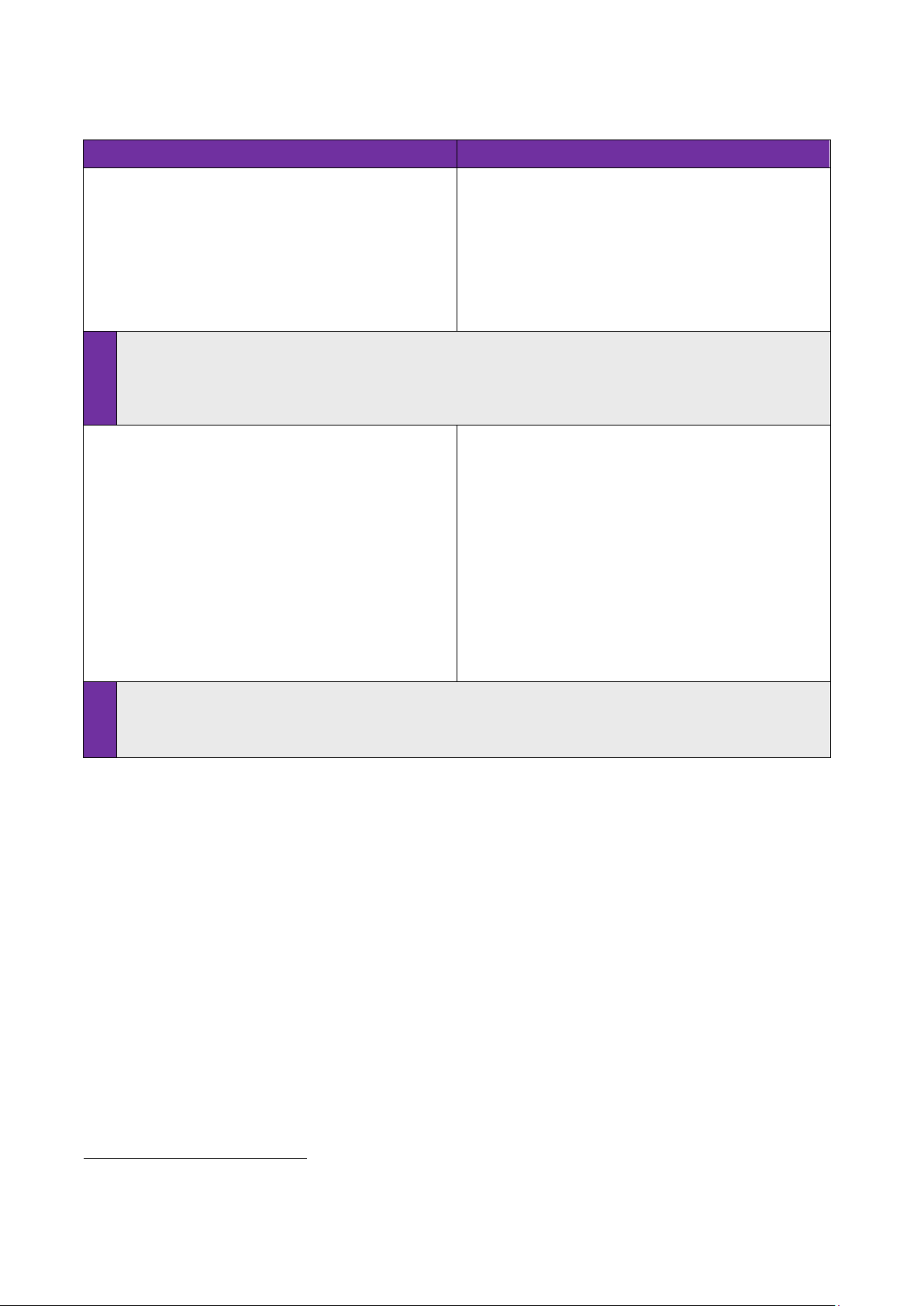

《3.シンガポール》

《(1) シンガポールにおける GAAS》

シンガポールと日本の GAAS を比較すると、主要な見解(key observations)に係る規定にほぼ

差異はない。

シンガポール 日本(参考)

【Singapore Standard on Auditing 701

4

(ISA701 から修正なし)】

A46. The amount of detail to be provided in the auditor’s report

to describe how a key audit matter was addressed in the audit

is a matter of professional judgement. In accordance with

paragraph 13(b), the auditor may describe:

• Aspects of the auditor’s response or approach that were most

relevant to the matter or specific to the assessed risk of

material misstatement;

• A brief overview of procedures performed;

• An indication of the outcome of the auditor’s procedures; or

• key observations with respect to the matter,

or some combination of these elements.

Law or regulation may prescribe a specific form or content for

the description of a key audit matter, or may specify the

inclusion of one or more of these elements.

【監査基準報告書 701】

A46.監査上の対応に関する記載の

詳細さの程度は、監査人の職業

的専門家としての判断に係る事

項である。監査人は、第 12 項(4)

に基づき、監査上の対応につい

て以下のいずれか、又は組み合

わせて記載する。

・ 監査上の主要な検討事項に

最も適合している、又は評価し

た重要な虚偽表示リスクに焦

点を当てた監査人の対応又は

監査アプローチの内容

・ 実施した手続の簡潔な概要

・ 監査人による手続の結果に

関連する記述

・ 当該事項に関する主要な見解

4

https://isca.org.sg/docs/default-source/audit-assurance/aa-standards/ssa-701-(dec-

2022)9d09920593614878a0bdccba5dc41a64.pdf?sfvrsn=c268da19_2

- 6 -

《(2) シンガポールにおける調査概要》

・ 調査対象の抽出

シンガポール証券取引所(Singapore Exchange:SGX)上場企業のうち、本社所在地がシンガ

ポールである企業 100 社を無作為に抽出した上で、それらの企業の KAM を調査し、監査人の主

要な見解等の記載の有無及び記載がある場合はその内容の分析を行った。

・ 調査結果概要

主要な見解(key observations)又は observations を記載している企業はなく、13%の企業

において findings が記載されていた。

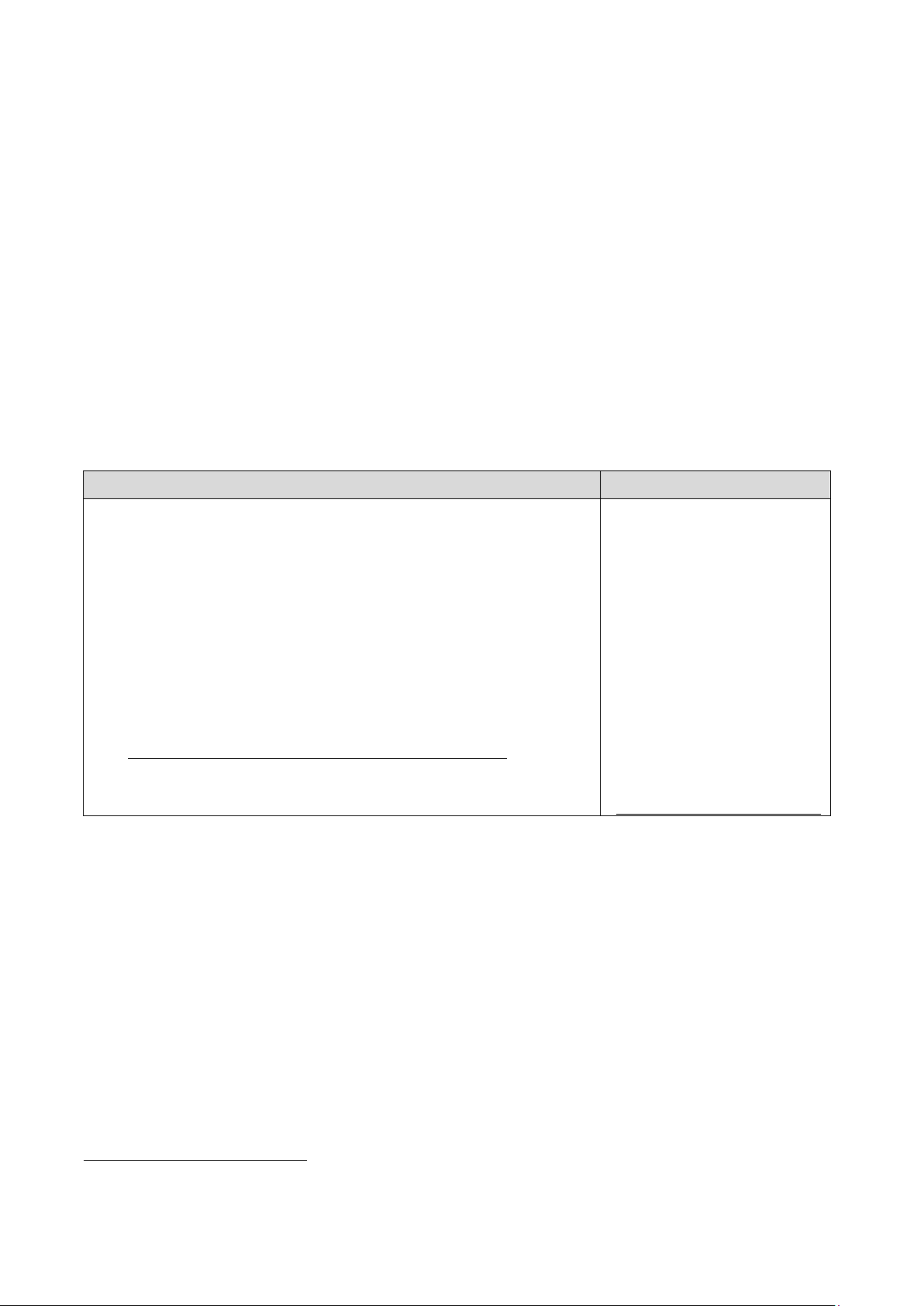

《4.米国》

《(1) 米国における GAAS》

米国と日本の GAAS を比較すると、主要な見解(key observations)に係る規定にほぼ差異はない。

米国 日本(参考)

【Auditing Standards AS 3101

5

】

14 For each critical audit matter communicated in the auditor's

report the auditor must:

a. Identify the critical audit matter;

b. Describe the principal considerations that led the auditor

to determine that the matter is a critical audit matter;

c. Describe how the critical audit matter was addressed in the

audit; and

Note: In describing how the critical audit matter was addressed

in the audit, the auditor may describe: (1) the auditor's

response or approach that was most relevant to the matter;

(2) a brief overview of the audit procedures performed; (3)

an indication of the outcome of the audit procedures; and (4)

key observations with respect to the matter, or some

combination of these elements.

d. Refer to the relevant financial statement accounts or

disclosures that relate to the critical audit matter.

【監査基準報告書 701】

A46.監査上の対応に関する記載の

詳細さの程度は、監査人の職業

的専門家としての判断に係る事

項である。監査人は、第 12 項(4)

に基づき、監査上の対応につい

て以下のいずれか、又は組み合

わせて記載する。

・ 監査上の主要な検討事項に

最も適合している、又は評価し

た重要な虚偽表示リスクに焦

点を当てた監査人の対応又は

監査アプローチの内容

・ 実施した手続の簡潔な概要

・ 監査人による手続の結果に

関連する記述

・ 当該事項に関する主要な見解

《(2) 米国における調査概要》

・ 調査対象の抽出

米国上場企業のうち、本社所在地が米国である企業 100 社を無作為に抽出した上で、それら

の企業の監査上の重要な事項(Critical Audit Matters:CAM)を調査し、監査人の主要な見解

等の記載の有無の調査を行った。

・ 調査結果概要

監査人の主要な見解等を記載している企業はなかった。

5

https://pcaobus.org/oversight/standards/auditing-standards/details/AS3101

- 7 -

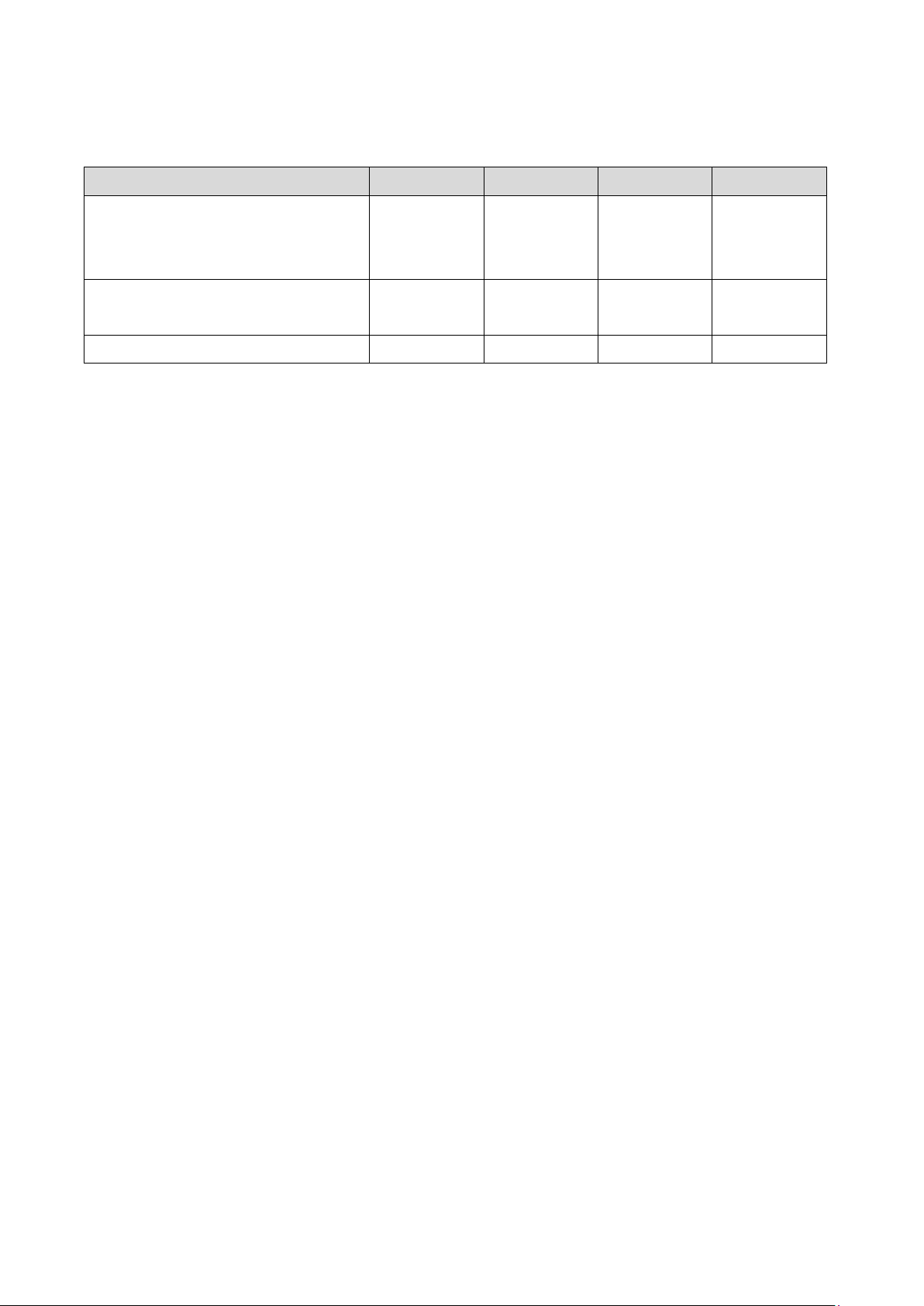

《5.まとめ》

《(1) 各国における調査結果まとめ》

英国 オランダ シンガポール

米国

主要な見解(key observations)又

は observations を記載している企

業

56 社

(56%)

76 社

(95%)

0社

(0%)

0社

(0%)

findings を記載している企業

4社

(4%)

0社

(0%)

13 社

(13%)

0社

(0%)

調査対象企業計

100 社

80 社

100 社

100 社

(注)( )内は、調査対象企業数に対する構成割合である。

《(2) 調査結果総括》

・ 監査基準又は規則において主要な見解(key observations)に関する追加の要求事項がある英

国やオランダにおいては、これらがない国と比べ、key observations 又は observations を記載

している事例が多く識別された。

・ 主要な見解(key observations)又は observations の事例の多くは「会計処理は適切である」

といった定型的な記載であった。また、個別意見を表明している印象を与える内容も多く見ら

れた。

・ 我が国と監査人の主要な見解に関する規定にほぼ差異がないと考えられるシンガポールにお

いては、主要な見解(key observations)又は observations を記載している事例はなかったも

のの、一部の企業において findings を記載している事例が識別された。

・ 我が国と監査人の主要な見解に関する規定にほぼ差異がないと考えられる米国においては、

監査人の主要な見解等を記載している事例はなかった。

- 8 -

《Ⅲ 調査結果を踏まえた考察》

調査対象とした国の全ての会社の開示内容を調査したものではないが、各国 100 社程度の開示

事例を調査した結果を取りまとめた。

《1.監査人の主要な見解等の記載の有無の傾向》

・ 主要な見解(key observations)の記載が多く見られた英国及びオランダにおいては、監査基

準や規則において主要な見解(key observations)に関する追加の要求事項が存在している。ま

た、これらの国においても、記載が必要と監査人が判断した場合に記載されるものとなってい

ることから、全ての KAM に主要な見解(key observations)が記載されているものではない。

・ 主要な見解(key observations)の記載が 100 件中 56 件と多く見られた英国においても、

findings の記載は4件と著しく少なかった。

・ findings の記載が比較的多く見られたシンガポールにおいても、100 件中 13 件と件数は少な

かった。また、findings を記載しているのは特定の監査事務所に集中している傾向が見られた。

・ 英国やシンガポールの findings の記載では、「監査人の判断(=XX は適切であるものと判断

した)」を記載しており、主要な見解(key observations)との線引きが非常に曖昧な状況のよ

うに見られた。

《2.監査人の主要な見解等の記載内容の傾向》

監査人の主要な見解等を記載している事例について、どのような内容が記載されているのかを

分析した。

・ 内容については、詳細に記載されているものがある一方、主要な見解(key observations)の

記載が多かった英国及びオランダにおいても、個別項目の検討の結果を一般的に記述するにと

どまっている記載や、結論が記載されているだけで、それ以外の付加的な情報はなく、定型文の

ような記載が多数見られた(海外事例1参照)。

・ 事実に即した監査結果の記載に該当せず、KAM に関連する勘定残高等についての結論を表明し

ているという印象を与える事例や監査手続の対象となった要素(経営者の重要な仮定や財務諸

表の開示)について監査手続の対象を具体的に特定した記述が十分ではない事例など、個別意

見を表明している印象を与える表現が見られると考えられる記載があった。一方、個別保証を

付与していない点を明記する等の記載も見られた(海外事例2及び3参照)。

・ 監査人が監査の過程で識別した事項に対応して、被監査会社の状況や監査アプローチの見直

しに言及した事例もあった(海外事例4参照)。

- IT全般統制の不備が継続している場合の記載

- 内部統制の不備への対応

・ KAM が監査委員会への報告事項であるから監査委員会の監査報告書を参照するといった、制度

設計の異なる国特有の事例もあった(海外事例5参照)。

- 9 -

《3.まとめ》

海外事例の調査分析を通じて、監査人の主要な見解等が多く記載されている国と我が国では監

査基準等が異なっていることが確認できた。

また、記載が充実している事例も見受けられたが、監査人の主要な見解等の記載が要求事項と

されている国においても、一般的で汎用的な記載が多く見られることが確認された。さらに、事実

に即した監査手続の実施結果の記載となっておらず、個別意見の表明をしているような印象を与

えると考えられるものも含まれていた。

このように、海外事例を読む限り、それぞれの読者において同一の表現に対して個別意見を表

明しているかどうかに関して異なる理解が生じており、個別意見を表明しているとの誤解を生じ

させる可能性が相当程度想定される。我が国より先行して KAM を導入した国においても、主要な

見解(key observations)については、財務諸表の利用者に対して有用かつ誤解を生じさせない記

述とは必ずしも言えず、また、監査人の主要な見解等において個別意見の表明を懸念させる表現

はどのようなものであるかが監査の基準において具体的に示されていない等、監査人に記載を促

す上で対応すべき重要な課題や論点がいまだ残されているものと考察する。

この点に関して、ISA701 においては、KAM の記載についてボイラープレート化することを避け

る観点から詳細な文例や制約は書き込まず原則主義の方針をとっており、監査手続の実施結果や

主要な見解等の記載に関してどのような表現が結論や意見の表明と誤解されるのかについて具体

的な事例等は示されていない。今後、ISA701 の適用指針等において取扱いが明らかにされること

が望ましいと思われる。

このような状況を踏まえると、我が国において監査人の主要な見解等の記載を行った場合、海

外事例と同様、個別意見の表明と誤認され得る記述がなされる可能性があり、また、個別意見の表

明と誤解されないよう留意すると、汎用的な記載となり、利用者にとって有用ではない情報提供

にとどまる可能性が高いのではないかと推察される。

一方、我が国においては、監査基準報告書 701 研究文書第1号「「監査上の主要な検討事項」の

早期適用事例分析レポート(研究文書)」及び監査基準報告書 701 研究文書第2号においても触れ

ているように、制度導入後、有価証券報告書における会社の開示内容は充実し、KAM の記載内容も

具体的な記載が増えてきている。

今後も監査上のリスクが高く重要であると考えられる事項については、財務諸表作成責任者で

ある経営者、ガバナンス責任者である監査役等と監査人の間で適切に協議することで、開示内容

とそれを受けての KAM の充実は図られていくものと考えられる。

日本公認会計士協会としては、「KAM の選定理由」や「監査上の対応」の記載について、対象と

なる会社並びに対象となる年度の事業内容及び事業環境を踏まえ、会社や事業固有の要因を含め

た具体的な記載を行うことを KAM の記載上の留意事項として、監査基準報告書 701 周知文書第2

号「監査上の主要な検討事項(KAM)の適用3年目に関する周知文書」(2023 年4月3日)を公表

し、強調しているところである。KAM の有用性を高めるために、まずは各監査人が「監査上の対応」

の記載において、監査の実施状況を個別具体的に記載することを継続して心掛けていくことが重

要である。その上で、アナリスト等の利用者からは findings 等による情報提供を期待する声もあ

ることから、主要な見解(key observations)や findings の記載が個別意見の表明との誤解が生

じず、かつ、利用者にとって有用な情報となるための記載の在り方については、国際的な記載実務

- 10 -

の動向も見据えながら、引き続き検討を行っていくことが望ましいと考える。

以 上

- 11 -

《Ⅳ 監査人の主要な見解等の海外事例》

《海外事例1.結論の記載以外の付加的な情報がない事例》

(種別:key observations)

英文 仮訳

We are satisfied that the

valuation of

XX assets and the related disclosures

are appropriate.

当監査法人は、XX 資産の評価と関連する開

示が適切であるとの心証を得た。

Based on our procedures we consider the

valuation of XX to be materially

appropriate.

当監査法人の手続に基づいて、当監査法人

は XX の評価が実質的に適切であると考え

る。

We concluded that the presentation of

revenue transactions is appropriate

and have been prepared in accordance

with IFRS 15.

当監査法人は、収益取引の表示は適切であ

り、IFRS 第 15 号に従って作成されている

と判断した。

▶ 結論が記載されているだけで、それ以外の付加的な情報はない(企業の開示が簡素なわけ

ではない)。

▶ 収益認識に係る不正リスクを KAM としている他社の事例でも、結論の根拠が記載されて

いるものは見受けられなかった(「……収益は適切に認識されている」、「重要な虚偽表

示は識別していない」、「報告すべき事項はない」等)。

- 12 -

《海外事例2.個別意見の表明であるような誤解を与える可能性のある事例》

(種別:key observations)

英文 仮訳

Based on the procedures performed, we

did not identify any material audit

findings in relation to the existence

or carrying values of the XX assets and

liabilities.

実施した手続に基づき、当監査法人は XX 資

産及び負債の実在性又は簿価に関連する

重要な監査上の発見事項を識別しなかっ

た。

Based on our audit procedures, we

consider Management’s judgements with

respect to the impairment review cash

flow assumptions to be reasonable and

achievable.

当監査法人の監査手続に基づき、当監査法

人は、減損レビューにおけるキャッシュ・

フローの仮定に関する経営者の判断は合

理的かつ達成可能であると考える。

▶ 資産の簿価に関連する重要な監査上の発見事項は識別されていないという記述が、特定

の勘定科目やアサーション(実在性)に対する個別意見の表明のような印象を与える可

能性がある

6

。

▶ 減損レビューにおけるキャッシュ・フローの仮定に関して監査手続の対象とした個々の

要素に関する評価ではなく、当該仮定が全体として合理的であるという監査人の判断を

記載しているため、結果として KAM の対象とした会計上の見積りに係る勘定科目に対す

る個別意見の表明のような印象を与える可能性がある

7

。

6

当該事例については、調査研究の過程で、「事実に即して監査手続の実施結果を記載したに過ぎず、個別意見を表明す

るものではない。」との意見が示された。しかしながら、他方では、「『重要な』といった様々な解釈を生じる用語を用い

ている点や、個々の監査手続の実施結果を記載しておらず、監査手続の目的(特定の勘定残高に係るアサーションの達

成)の達成状況を記載している点において、事実に即した監査手続の実施結果の記載とは言えない。KAM に関連する勘定

残高等についての個別意見を表明しているという印象を与える。」といった意見も見られた。

7

経営者の仮定が合理的かつ達成可能であることを検討した旨の記載事例がある。当該事例については、調査研究の過程

で、「監査上の対応として記載した監査アプローチ又は手続の対象となった要素(経営者の重要な仮定等)に対する監査

人の評価を記述したものであり、個別意見を表明するものではない。」との意見が示された。しかしながら、他方では、

「経営者の重要な仮定等に含まれる個々の要素(例えば、キャッシュ・フローの成長率)を具体的に特定して記述していな

いため、監査手続の対象となった要素に対する評価を記載するという実務ガイダンスの取扱いを逸脱している。『減損レ

ビューにおけるキャッシュ・フローの仮定や投資の回収可能性に対するに関する経営者の判断が合理的である』という記

載は、監査手続の目的の達成状況を示しており、減損の会計処理に対して個別意見を表明しているという印象を与え

る。」という意見があった。また、「財務諸表の適正表示ではなく『キャッシュ・フローの仮定が達成可能であるかどう

か』について個別の保証を付与しているように読める」という意見も見られた。

- 13 -

(種別:findings)

英文 仮訳

We found Management’s appraisal of the

recoverability of the Company’s

equity investments in

subsidiaries,

associated and joint venture companies

to be appropriate. We also found

disclosures in the financial

statements to be appropriate.

当監査法人は、子会社、関連会社及び合弁

会社に対する投資の回収可能性に関する

経営者の評価が適切であると判断した。ま

た、財務諸表における開示も適切であるこ

とを確かめた。

▶ 監査手続の対象とした個々の要素に関する評価ではなく、経営者の評価及び財務諸表の

開示に対する監査人の全体としての評価を記述しているため、関連する勘定科目におけ

る特定のアサーション(評価)及び財務諸表における開示について、個別の意見を表明

しているという印象を与える可能性がある

8

。

We found that the assumptions were

applied appropriately, reflected

comparable market transactions (where

available and

appropriate) and

included consideration of the impact

of climate change and a range of other

external factors. Where assumptions

did not fall within our expected range,

we were satisfied that the variances

were due to property specific factors

as noted above.

当監査法人は、仮定が適切に適用され、(入

手可能で適切な場合には)比較可能な市場

取引を反映し、気候変動の影響やその他

様々な外部要因の考慮が含まれているこ

とを確かめた。当監査法人は、仮定が我々

の予想した範囲内に収まらなかった場合

には、上記にある物件固有の要因から生じ

る差異であることの心証を得た。

▶ 前提条件が監査人の予想に収まらなかったケースについて記述している。

▶ 「固有の要因」の具体的な内容や、固有の要因の相当性に対する具体的な対応手続の記

載はなく、手続実施結果の記載としても十分な記載ではない印象を与える。

8

脚注6と同様。

- 14 -

《海外事例3.個別保証を付与していない点を明記している例》

(種別:key observations)

英文 仮訳

We addressed the key audit matters in

the context of our audit of the

financial statements as a whole, and

in forming our opinion thereon. We do

not provide separate opinions on

these

matters or on specific elements of the

financial statements. Any comment or

observation we made on the results of

our procedures should be read in this

context.

We concur with management, regarding

XXX that the calculations, accounting,

presentation and disclosures are in

line with the agreement and are

performed in line with IFRS.

当監査法人は、監査意見表明の基礎となる

財務諸表全体の監査において、監査上の主

要な検討な事項について検討した。当監査

法人は、これらの事項又は財務諸表の特定

の要素について個別に意見を表明するも

のではない。我々の手続の結果について

我々が行ったコメントや見解は、この文脈

で読まれるべきである。

当監査法人は、XXX に関して、計算、会計

処理及び開示が契約に従っており、IFRS に

従って行われていることについて、経営者

に同意する。

▶ 個別保証は付与していない点を明記している。

▶ ただし、続く文章で、計算、会計処理及び開示といった一連の取扱いについて経営者に

同意する旨を記載しており、個別意見を表明している印象を与える記述である。

- 15 -

《海外事例4.監査人が識別した事項及びそれに対応する監査アプローチに言及した事例》

(種別:key observations)

英文 仮訳

In 20XX management remediated the

observations, as shared by us in

previous years, in relation to the

general IT controls. During 20XX, next

to design and implementation, we also

tested operating effectiveness of the

general IT Controls to determine

whether the controls were working

effect

ively throughout the year. Due

to identified deficiencies we were not

able to rely on the general IT controls

for the audit of 20XX. As a result we

applied a substantive audit approach.

20XX 年、経営者はIT全般統制に関して、

前年に当監査法人が共有した指摘事項を

修正した。 20XX 年には、デザインと適用

に加えて、IT全般統制の運用の有効性も

テストし、コントロールが年間を通じて有

効に機能しているかどうかを確認した。不

備が特定されたため、20XX 年の監査ではI

T全般統制に依拠できなかった。そのた

め、実証的な監査アプローチを適用した。

▶ 監査アプローチの説明の中で、企業のIT全般統制の不備について記載している。

▶ 被監査会社に指摘し、被監査会社が年々改善に取り組んでいるが、まだ依拠できるレベ

ルにないことを示している。

We have identifi

ed a number of

deficiencies,

including a lack of

evidence considered in key management

review controls, including those over

complex assessment contracts. Overall,

we consider that the control

environment requires signifi

cant

improvement to decrease the number of

misstatements identifi

ed. We

appropriately increased the extent of

our audit procedures to address the

risks identified

当監査法人は複雑な評価契約を含む主要

なマネジメントレビューコントロールに

おいて考慮される証拠の欠如等、多くの不

備を識別した。全体として、識別される虚

偽表示の数を減らすために、統制環境には

大幅な改善が必要であると判断した。当監

査法人は、識別されたリスクに対処するた

めに、監査手続の範囲を適切に拡大した。

▶ 監査アプローチの説明の中で、企業の内部統制の不備について言及した上で、被監査会

社の要改善課題の存在を示している。

▶ KAM の記載の中では、監査対応の範囲の拡大についても言及されている。

- 16 -

《海外事例5.監査委員会の監査報告書において強調した事項を記載した事例》

(種別:key observations)

英文 仮訳

Although the estimation of the expected

credit loss is by nature highly

judgmental

, based on the results of our

audit procedures, we concluded that the

ECL provision is appropriate as at 31

XX 20XX. Specifically, we emphasized

the following to the Audit Committee:

We considered the overall valuation

and treatment of collateral to be

materially reasonable, but noted

there is increased judgment regarding

the timing of realization in the

current environment.

Staging, inputs and assumptions are

appropriately applied to the ECL

calculation.

Financial statements disclosures on

loans and receivables and the ECL

allowance are in accordance with the

requirements of IFRS 9.

予想される信用損失の見積りは内容的に

高度な判断力を伴うものであるが、当監査

法人の監査手続の結果に基づき、20XX 年 XX

月 31 日時点で、予想信用損失に対する引

当金は適切であると判断した。とりわけ、

次の点を監査委員会に強調した。

当監査法人は、担保の全体的な評価と取

扱いは実質的に合理的であると考えた

が、現在の環境では認識のタイミングに

ついての判断が高まっていることに留意

した。

ステージング、インプット及び仮定が予想

信用損失の算定において適切に適用され

ていた。

貸付金及び債権、並びに予想信用損失に

対する引当金に関する財務諸表の開示

は、IFRS 第9号の要求事項に準拠してい

る。

▶ 結論の記載だけでなく、監査委員会の監査報告書において強調した事項が記載されてい

る。

以 上